Water quality: treatment, regulation and innovation

Water utilities are making long-term treatment decisions inside an uncertain regulatory environment, and PFAS — per- and polyfluoroalkyl substances (PFAS), commonly known as “forever chemicals” — is an example. Financial capacity has overtaken regulatory uncertainty as the top barrier among utilities addressing PFAS, with 31% of respondents citing budget and ratepayer constraints as the greatest limiting factor. Only 24% are confident in meeting regulatory obligations without substantial rate increases.

Regulation remains the dominant force shaping capital plans — 61% say regulatory changes are driving capital planning significantly or moderately — and most have responded by reallocating funds, slowing capital improvement program (CIP) projects or setting aside contingency.

Operationally, two-thirds of respondents point to treatment upgrades as the top challenge, compounded by generational workforce turnover reshaping skill sets and training needs.

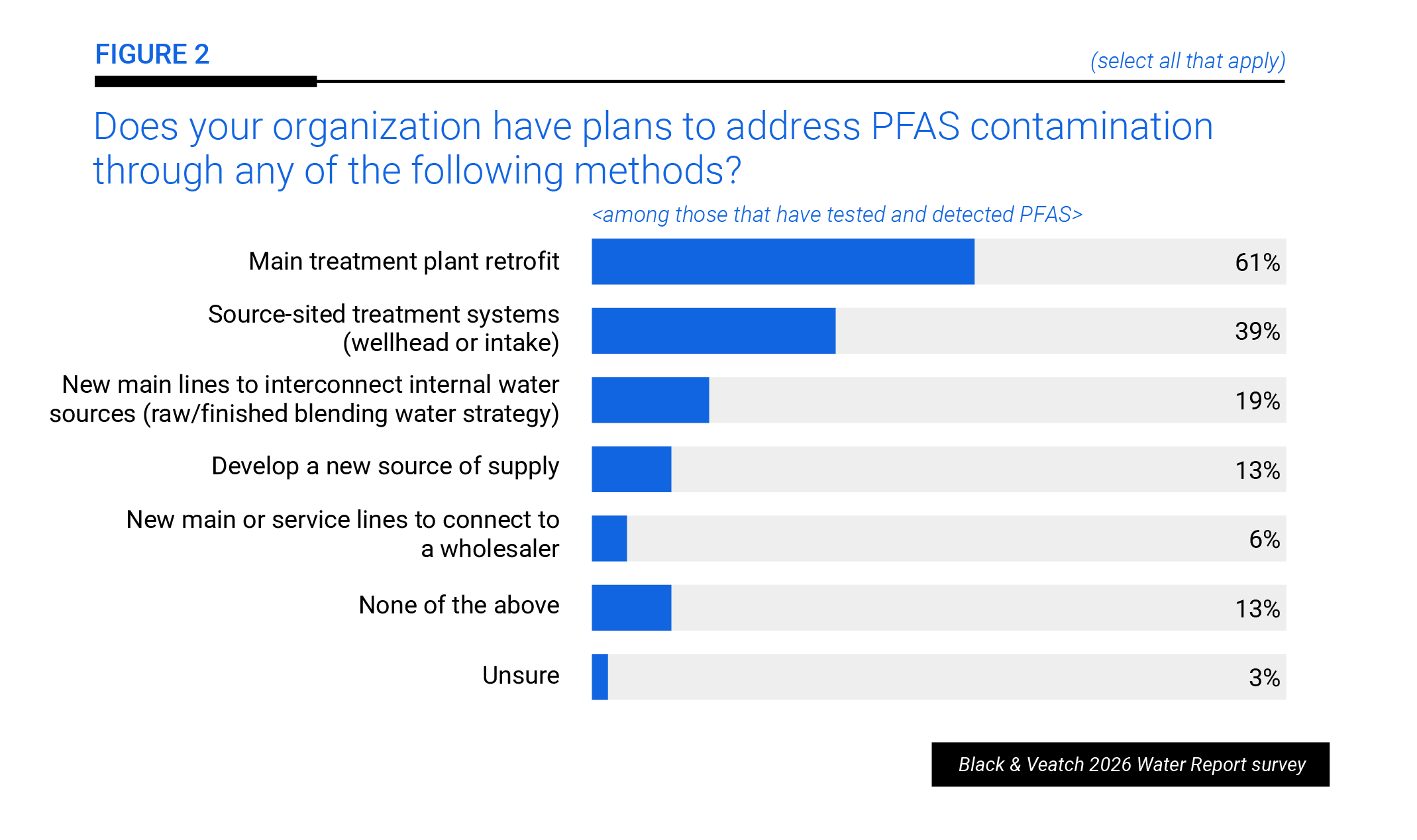

The solutions being leveraged to such water quality challenges, needs and goals show strategic thinking. Despite regulatory uncertainty, 35% of drinking water respondents are planning or implementing PFAS treatment, and among those with plans, 61% are pursuing main treatment plant retrofits (Figure 2).

The proactivity extends across the treatment spectrum: 80% of wastewater respondents report testing influent, effluent or biosolids for PFAS. Utilities are holding back on microplastics, an emerging contaminant quickly garnering attention. They’re preserving capital for more near-term and clearer compliance mandates.

The bottom line: Utilities are tackling risks directly, investing and innovating where the return is clearest, balancing compliance, sustainability, resilience and practicality.